Practical Greenhouse Gas (GHG) Inventory Steps That Build Resilience & Value

A robust greenhouse gas (GHG) inventory is becoming a tool for resilience, cost performance, and risk management, not just compliance. Many organizations are managing inventories voluntarily to strengthen stakeholder trust, meet customer or funder expectations, and guide practical cost and risk decisions—even when reporting isn’t required.

A robust greenhouse gas (GHG) inventory is becoming a tool for resilience, cost performance, and risk management, not just compliance. Many organizations are managing inventories voluntarily to strengthen stakeholder trust, meet customer or funder expectations, and guide practical cost and risk decisions—even when reporting isn’t required.

To get started, senior leadership can use accurate Scope 1 and Scope 2 data, and prioritize Scope 3 data to strengthen oversight, inform strategy, and build stakeholder trust. A phased approach can help you develop a program that focuses on impact, value, and credibility.

Key Concepts of GHG Inventory

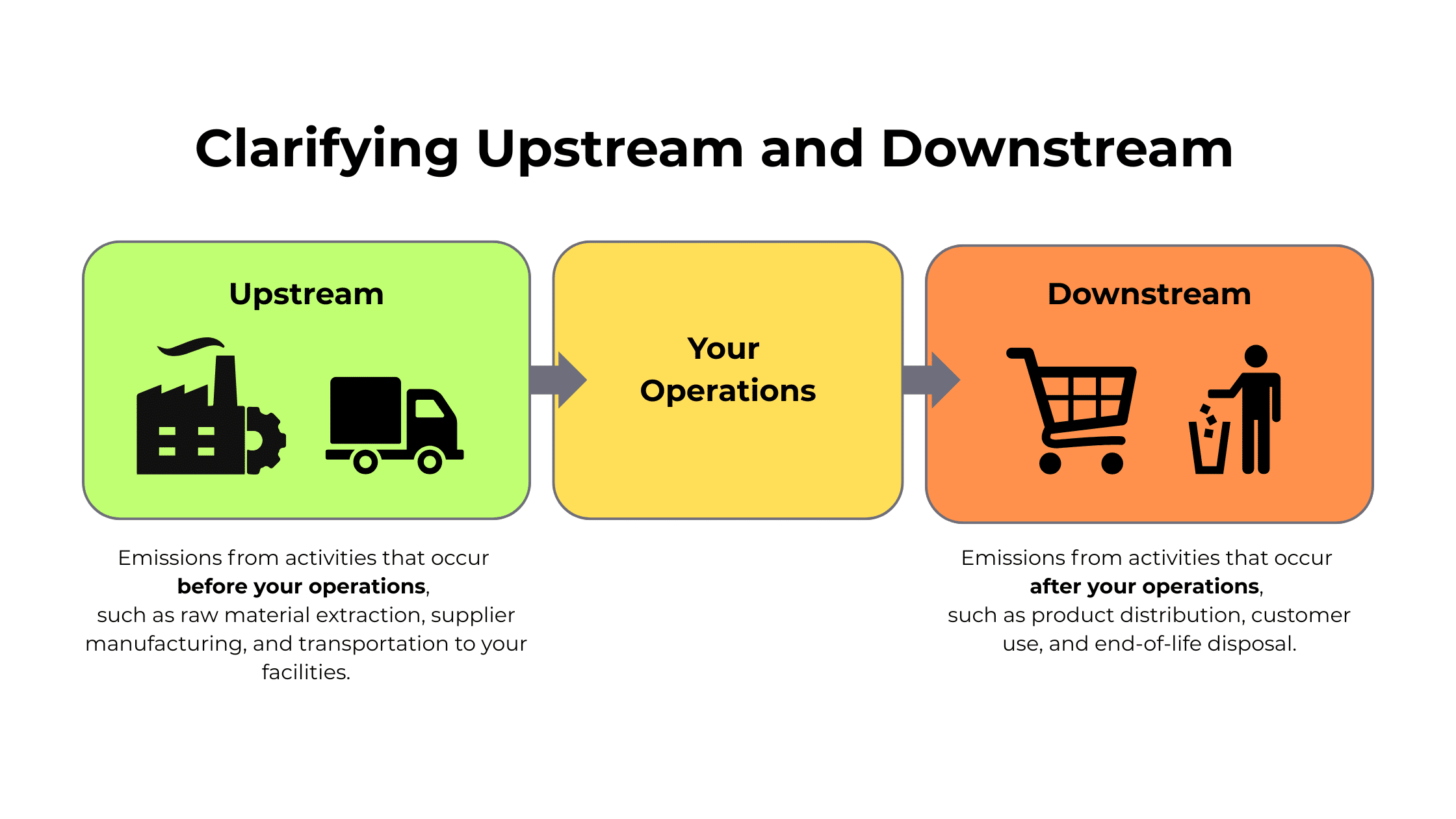

A GHG inventory categorizes emissions into three scopes:

- Scope 1 (Direct): Emissions from sources owned or controlled by the organization (e.g., onsite fuel combustion, company vehicles).

Why it matters: these emissions are most controllable and tracking them offers a reliable starting point. - Scope 2 (Indirect Energy): Emissions from purchased electricity, steam, heating, or cooling.

Why it matters: organizations can influence these through efficiency and renewable procurement. - Scope 3 (Other Indirect): Emissions across the value chain (upstream and downstream).

Why it matters: these emissions are often the largest share and the hardest to quantify, so prioritization and supplier collaboration are key.

For more in-depth explanation, read our article, “Greenhouse Gas Emissions: Understanding and Reporting on Scopes 1, 2, and 3.”

Why GHG Inventory Matters

Disclosure expectations are strengthening globally, including in the U.S., where requirements are evolving.

In California, Senate Bill 253 (SB 253), the Climate Corporate Data Accountability Act, mandates that large U.S. companies doing business in California with over $1 billion in annual revenue must publicly disclose their annual Scope 1, 2, and 3 greenhouse gas (GHG) emissions. SB 253 remains on track with the first Scope 1 and Scope 2 report now due August 10, 2026, with flexibility around first‑year assurance. However, Senate Bill 261 (SB 261), which requires large companies doing business in California to publish biennial reports on their climate-related financial risks, is stayed pending appeal. The California Air Resources Board is not enforcing the January 1, 2026 date while the stay is in effect.

In the EU, the Corporate Sustainability Reporting Directive (CSRD) significantly expands mandatory sustainability reporting for roughly 50,000 companies in scope, though thresholds and timing continue to evolve.

Regulations are one driver, but they’re not the only reason organizations build a GHG inventory. Many do so voluntarily to improve decision-making, strengthen stakeholder trust, and respond to customer, partner, or funder expectations. A credible inventory helps meet these current and anticipated regulatory requirements, surface cost and operational hotspots, enable science‑based targets, and reinforce trust with transparent, decision‑useful reporting.

Getting GHG Inventory Right: Foundations, Focus, and Integrity

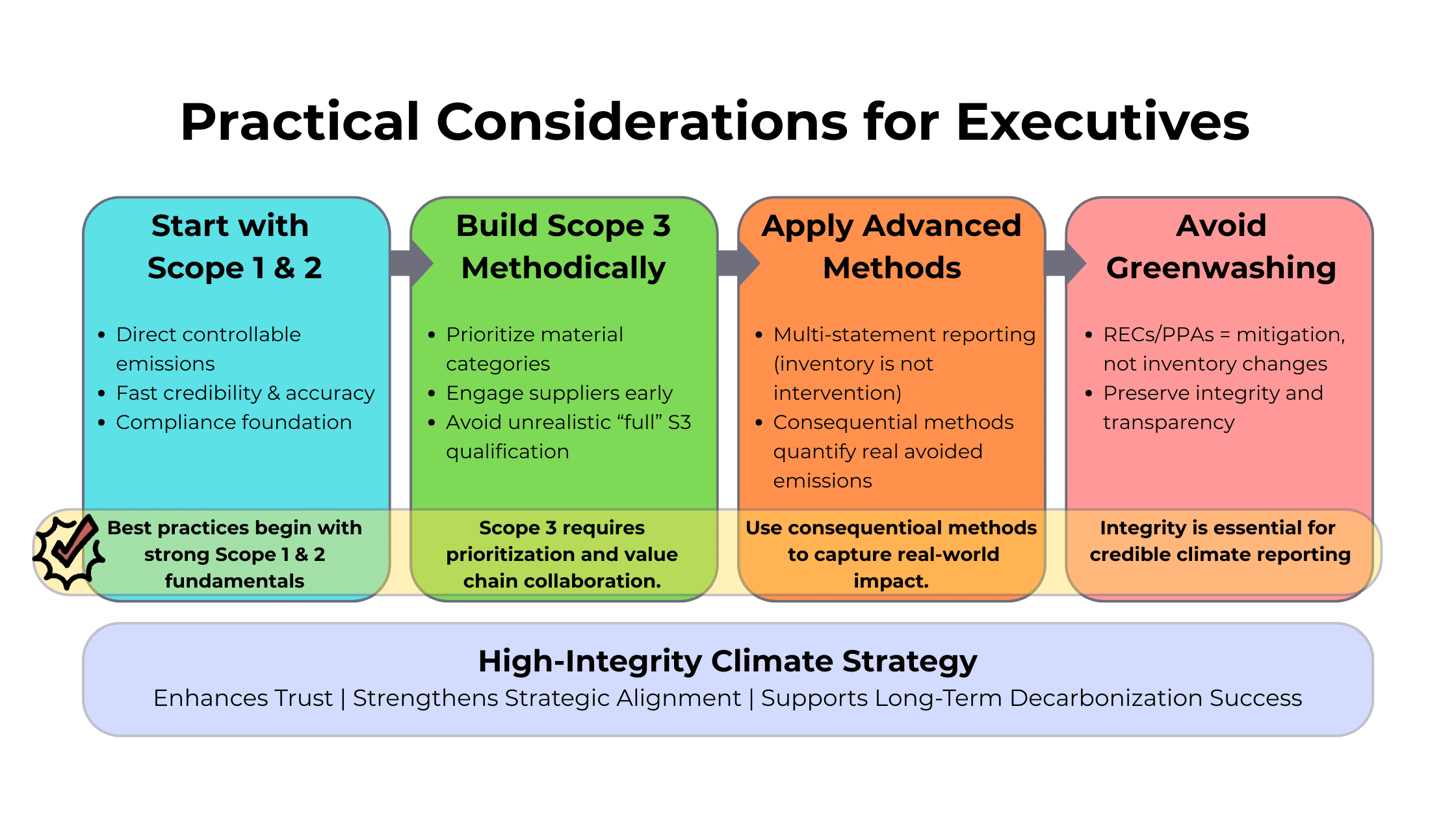

Start by establishing a strong foundation through Scopes 1 and 2, where emissions are most directly measurable and progress is easily auditable. As you expand into Scope 3, a methodical approach is essential, focusing first on the most material categories, incorporating supplier specific data whenever possible, and relying on conservative default values where data gaps persist.

Maintaining integrity throughout the process is critical. We recommend using market-based instruments such as renewable energy certificates (RECs) and power purchase agreements (PPAs) strictly as mitigation tools rather than substitutes for actual physical emissions. This avoids “greenwashing” (claims that overstate real-world emissions reductions or rely on accounting-only substitutions).

As maturity grows, your organization can advance to multi-statement reporting (separating “actual emissions” from “mitigation actions”) and consequential analysis (estimating the downstream effects of interventions), enabling you to clearly distinguish core inventory accountability from the broader impacts of their mitigation interventions.

Why It Matters for Resilience & Value

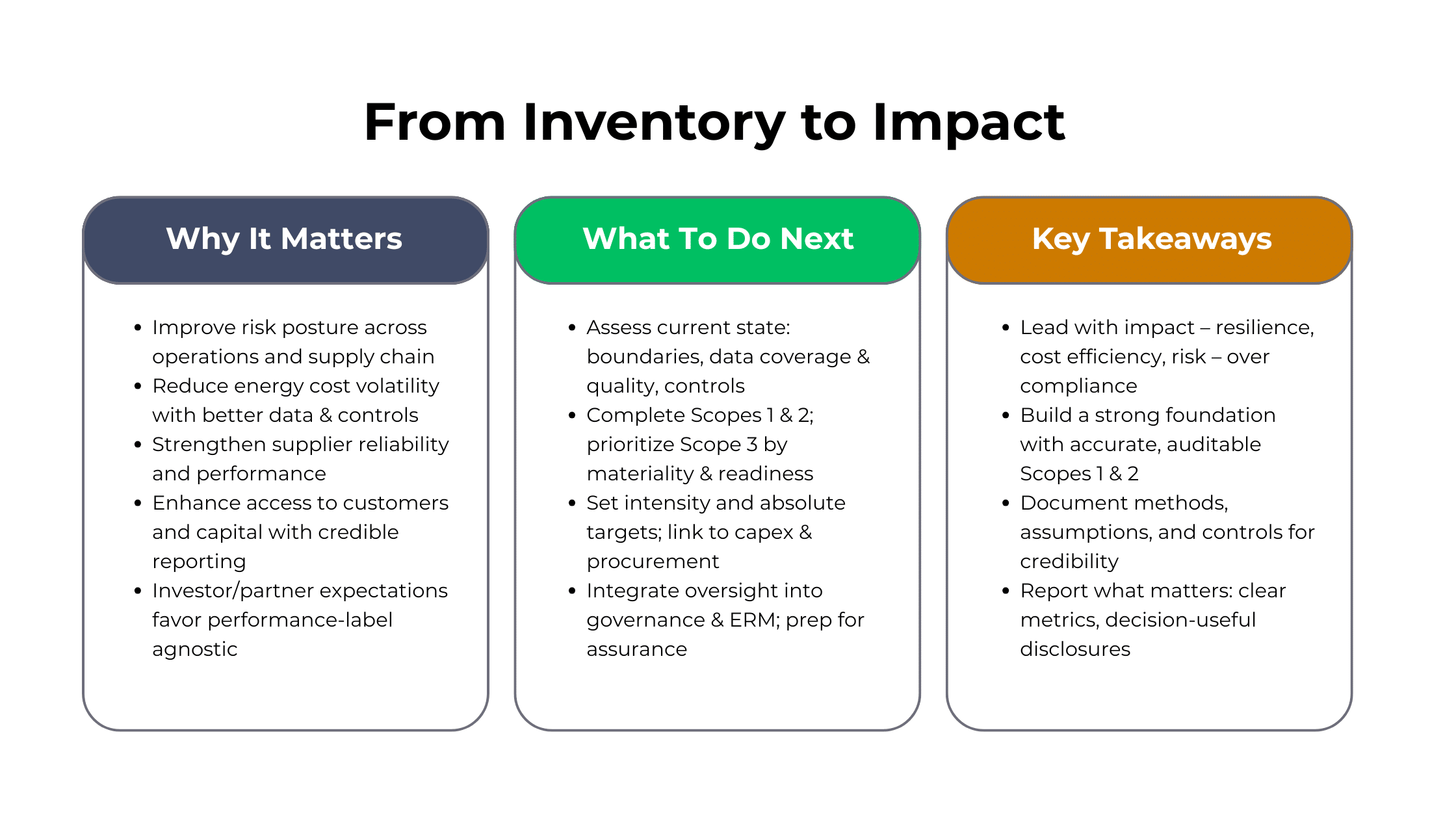

Organizations that embed GHG management into operations and governance improve their risk posture, reduce energy cost volatility, strengthen supply‑chain reliability, and enhance access to customers and capital. Investor and partner expectations continue to favor credible climate performance, regardless of the label applied (ESG, impact, resilience).

Higher quality voluntary carbon disclosures are linked to a lower cost of equity, and many organizations report improved access to capital as their climate reporting strengthens. Clear, defensible emissions data also supports grant and partner requirements for nonprofits and public sector entities, particularly as some state programs now mandate GHG inventories. Because Scope 3 emissions often highlight supply chain risks, organizations that actively engage suppliers can enhance data quality while improving overall value chain resilience.

What Leaders Should Do Next

Begin by assessing your organization’s current state, including inventory boundaries, data coverage and quality, and the strength of your internal control environment. With this baseline in place, you can complete comprehensive Scopes 1 and 2 assessments while prioritizing Scope 3 categories based on materiality and data readiness.

From there, leadership should set both intensity-based and absolute performance targets and directly link those goals to capital planning and procurement decisions.

Finally, integrate oversight into governance and enterprise risk management agendas, preparing for external assurance even before it becomes mandatory. This ensures long-term accountability and positions your organization for future regulatory developments.

Key Takeaways for Executives

As a leader at your organization, you can start by focusing your climate efforts on resilience, cost efficiency, and risk management rather than treating sustainability as a compliance exercise. A strong foundation begins with accurate and auditable Scope 1 and 2 reporting, followed by a disciplined and strategic approach to scaling Scope 3 based on materiality and data readiness.

Clearly document your methodologies, assumptions, and controls to maintain credibility and ensure that reported information aligns with recognized best practices seen across sustainability reporting frameworks.

Finally, focus your reporting on what truly matters, using clear metrics, decision-useful disclosures, and well supported narratives that can withstand internal review and future assurance expectations.

GRF Can Help

GRF’s approach is designed to be a lighter lift for you: we help define boundaries, collect and normalize available data, perform the emissions calculations, and document assumptions and controls so the inventory is audit ready. This work can be delivered as a standalone engagement or integrated into broader impact reporting or double materiality/ERM efforts, depending on your goals.

We are ready to support your organization as you address the growing expectations around GHG reporting and climate accountability. If your organization is preparing to strengthen its emissions inventory, enhance governance oversight, or develop a credible impact strategy, our ESG / Impact Services team is here to help. Connect with us to begin building a practical, reliable, and forward-looking approach to your climate and sustainability reporting.